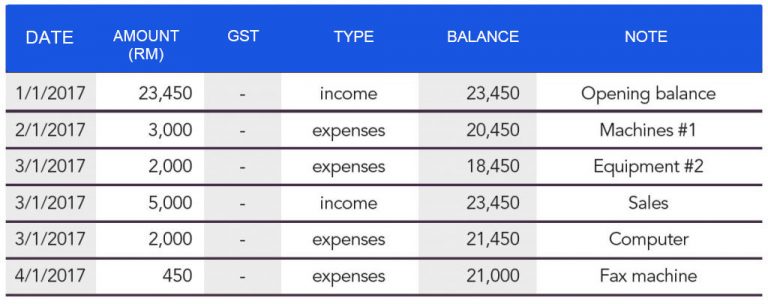

The basic accounting system would be keeping a cashbook record. It is important to keep all your record of expenses and original documents such as bills, invoices, receipt, payment and sales voucher as a proof of the statement of your entry in your cashbook. From this cashbook, later on, you will transfer all the data to your business account for the monthly statement. For small business entrepreneurs normally they just use a cashbook to manage their daily transaction.

This Toolkit will teach you how to prepare and maintain a simple cashbook recording. The cashbook will help to analyze your income and as well as determine your tax and GST returns. A good cashbook can be in a manual or electronic format, but must be easy to use and does not take up too much of your time to understand. The manual cashbook example explained here serves as a guide, shows a few entries, but understanding its operation will give you a basic understanding of a computerized cashbook.